Google in 2004.

The End.

Okay, But Really…

There is a multitude of different investments you can make, all with varying degrees of risk, return, and liquidity. In the investment world, we weigh these three factors against each other constantly to determine the correct percentage of your portfolio to allocate to each type of investment. Generally, the riskier an investment, the higher the potential payout. The number one investment you can make; however, far exceeds the return of any other market-based investment?

High return with very little risk? It sounds suspicious, but it’s true! The one investment you can make that produces more value than any other is your children. Proactively investing in future generations has no risk and limitless return. Not as an investment for direct monetary gain, unless you propagate the next Zuckerberg or Musk, but rather in connection. The real “Return On Investment” is more about human relationships than money. I am talking about value and time. Most people would agree that kids are more valuable than any amount of money and worth a solid investment of time into and money. While the “return” itself is not exactly measurable, there is a strong argument that your ROC (Return On Children) will provide you with more value than any portfolio ROI ; after all, they are your number one investment.

College Debt, The Opportunity Killer

Student loans have continued to increase, and they’ve never been higher.

According to Forbes, the total student loan debt in the US is just over $1.5 trillion dollars (2019). When the numbers get this large, it’s hard to put into perspective. For reference, a trillion dollars is taking a million dollars, and multiplying that by another million… In short, that’s a lot of student loans.

Assuming the average loan interest rate is 5.8%, paying off these loans is essentially providing a guaranteed annual return of 5.8%

Your Family and Legacy

The importance of your legacy and your children’s future shouldn’t be underestimated. They are the future of the entire world… No pressure… Why does that matter? Well, if you consider yourself to be the most important person in your life then I suppose it doesn’t, but if you care about your children more than yourself, make sure your focus on ROK exceeds your ROI focus. Uncertainty is a part of life we have always faced when it comes to the future, it is important to set the next generation up with as many opportunities and as possible.

Start with Yourself

Slow down, before you start thinking about handing over all your money to your kids, make sure that you yourself are financially secure. First, have your own portfolio in order. How does that line go? In the event of an emergency secure your oxygen mask before helping others with theirs. This concept certainly applies to more than just bags that fall from the roof of airplanes. Financial security is more than having enough money or even more than enough money. It’s about having your money and assets in the right places. Understand the relevance of market trends, statistical data, current economic events, and how to deal with the uncertainty that our economy faces so that your future generations can be set up for the brightest future, or make sure you have a really good and trustworthy pilot.

Saving for Retirement Vs. Saving for Your Child’s Education

Many parents struggle with deciding how much they should be saving for their retirement vs. how much they should set aside for their children’s education. The first thing to wrap your arms around is the different lengths of time before each event will occur and how long it will last. If your child is a 1-year-old, you typically have an 18-year time horizon with a four-year college term. Similarly, in how many years would you like to retire and how what’s your estimated longevity? As expensive as college can be, there are more than enough ways to pay for it, including grants, scholarships, loans, military, work-study, or you can just go FU** Yourself. Retirement, on the other hand, is up to the retiree to fund above social security. If money is tight, you should focus on your retirement funds if you don’t want to rely on your children’s support. On the other hand, if you are diligent with your personal savings and retirement funds, planning for your child’s future and teaching them good habits is an invaluable investment.

Creating a Plan

As important as it is to invest time into your children to teach them, nurture them, and help them grow, setting aside money for them can be a great idea. Having enough money to send your child to school doesn’t just happen by chance, however. A study from Sallie May in 2018 shows that parents with a structured, well-advised savings plan for their children’s education have over double the savings than those without a plan by the time their child goes to college. This is good news since you know your number one investment and you’re a responsible parent looking to set your child up for success. This is no surprise and can easily be applied to any other monetary goal that you may have. Plans work, especially ones that have data supporting their success.

The 529 Plan

We know that you want the best for your kids. You most likely want to give your kids the world, or at least provide them the ability to become a productive self-sufficient member of society. Opening a 529 is a good source to help them open doors. Qualified Tuition Plans (529 plan) are state-sponsored savings plans designed for future education costs. Residence from all 50 states can begin investing in these plans. Here are the benefits, and why you might want to consider a 529 for your child’s future education.

• There are no restrictions on age or income

• You have full control over your investment

• Other individuals can contribute gifts into the account

• The beneficiary can change one time/ year and can even be a non-related 3rd party.

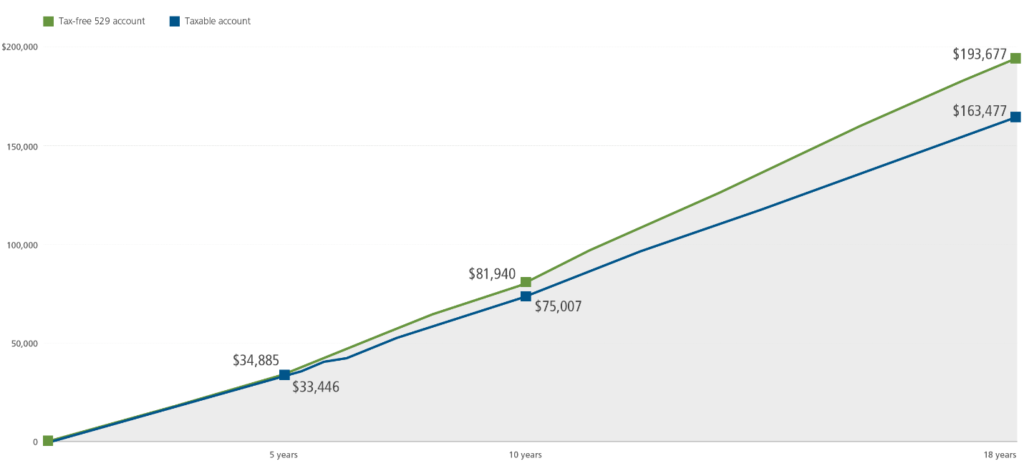

• Most importantly – tax advantages – As long as the money ends up being used for qualified tuition expenses (tuition, room and board, computers, textbooks, other fees), it grows federally tax-free, and is not taxed when withdrawn. See the graph below.

A hypothetical account with a $500 monthly contribution growing at 6% and assuming a 28% tax bracket.

(Disclaimer- These are hypothetical numbers for visualization purposes only. This graph is not illustrative of any particular return from a specific account and is not intending to predict the outcome of any future 529 investments.)

To learn more about 529 plans, schedule a video conference with a Demand Wealth planner.

Each generation has a responsibility to the next. Your number one investment has extraordinary value. Investing in them is more than simply saving for their education. It’s about setting an example while teaching them important values and money responsibility. Having and raising children, teaching them, and saving money for their education is more than an investment, it’s both a sacrifice and a blessing. You want what’s best for your kids, investing so much time, money, and effort to raise them right so they can be set up for as many opportunities as possible. We aren’t talking about specific stocks, bonds, and numbers, we’re talking about value and love. Investing in the next generation is the #1 investment you can make. After all, investing was never about the sensationalism of today, it’s about the future.